After eight years of waiting, the GST Appellate Tribunal (GSTAT) is finally operational. Formally launched by Finance Minister Nirmala Sitharaman on September 24, 2025, the tribunal commenced adjudicatory operations on February 16, 2026, with the Principal Bench in New Delhi and several state benches now hearing cases.

For businesses, this means one thing: if you have an adverse GST order from the First Appellate Authority that you’ve been unable to challenge because the tribunal didn’t exist, your window is now open. And it closes on June 30, 2026.

At PGA & Co., our GST litigation team is currently helping businesses across Chandigarh, Delhi NCR, and Punjab prepare and file GSTAT appeals. This guide walks you through the entire process — from eligibility to filing to what happens after.

Why This Matters: The Numbers

GSTAT President Justice Sanjaya Kumar Mishra has stated that 5.82 lakh cases have already been decided at the first appellate stage. Around 2 lakh appeals are expected to be filed before the tribunal by June 30, 2026. If your case is among them and you miss the deadline, you permanently lose the right to second appeal.

Who Can File an Appeal Before GSTAT?

Any person dissatisfied with an order passed by the First Appellate Authority (Commissioner Appeals) under Section 107 or the Revisional Authority under Section 108 of the CGST Act can file an appeal before GSTAT. This includes:

• Registered taxpayers (companies, LLPs, firms, proprietorships) who received adverse demand orders

• E-commerce operators facing TCS demand confirmations

• Exporters whose refund rejection appeals were dismissed

• Input Service Distributors with ITC reversal orders confirmed on appeal

Important threshold: GSTAT cannot admit an appeal where the total tax, interest, fine, fee, or penalty involved is less than ₹50,000 (Section 112(1)).

The Deadline: What “June 30, 2026” Actually Means

For all orders communicated before April 1, 2026, the absolute cut-off to file before GSTAT is June 30, 2026. The tribunal can condone a delay of up to 3 additional months if you show sufficient cause — but this is discretionary, not guaranteed.

For orders communicated on or after April 1, 2026, the standard 3-month limitation period applies from the date of communication.

Critical point: Filing is only considered valid when the Final Acknowledgement (Part B of Form GST APL-02A) is issued. A provisional acknowledgement alone is not enough. If there are defects in your filing, the appeal won’t be admitted even if you submitted before June 30. Start early.

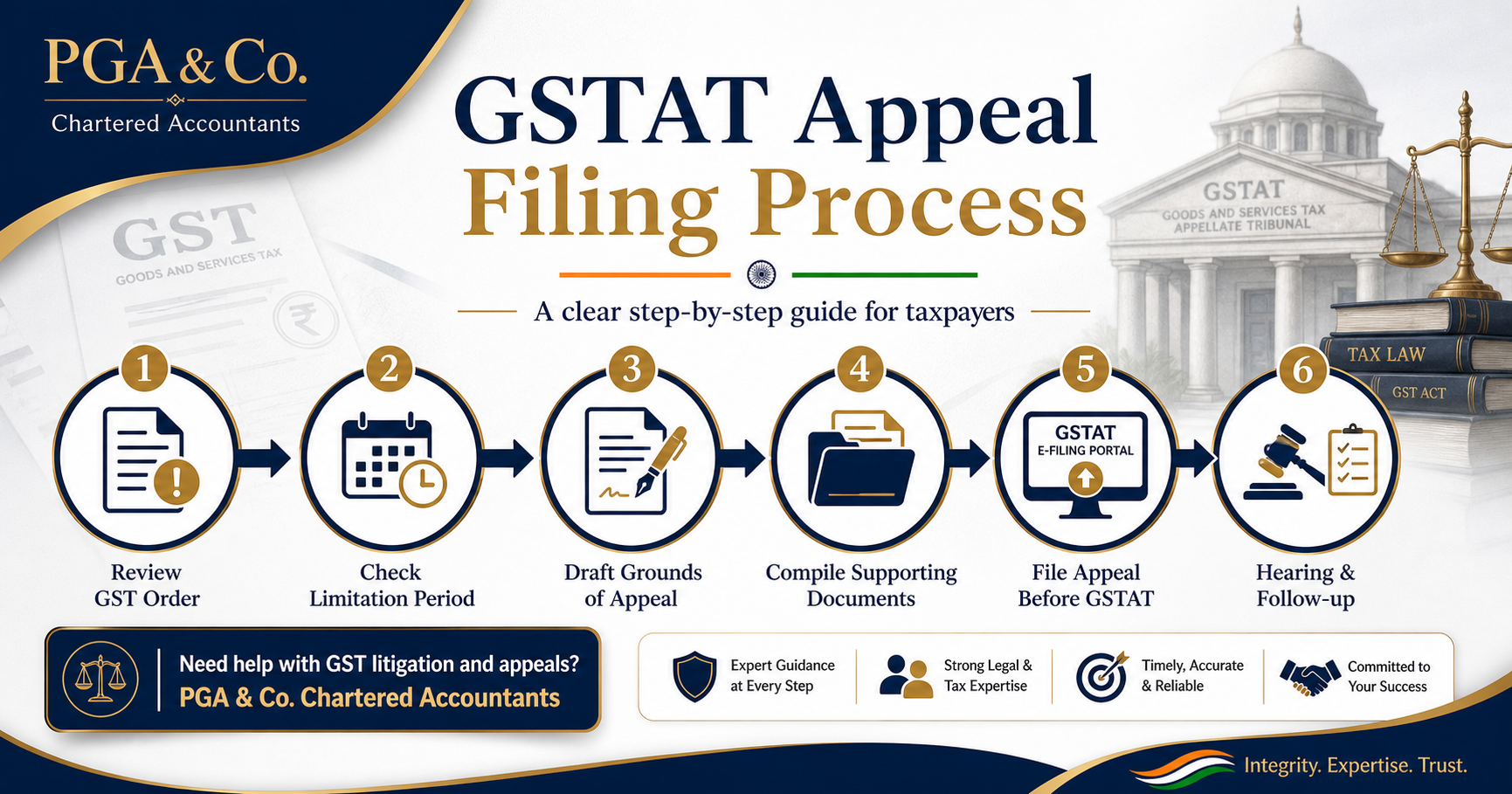

Step-by-Step: How to File a GSTAT Appeal

Step 1: Assess Whether Your Case Is Worth Appealing

Before investing time and the mandatory pre-deposit, evaluate your case objectively:

• Is the legal position in your favour based on existing High Court or Supreme Court precedents?

• Was the First Appellate Authority’s order unreasoned or did it ignore evidence you submitted?

• What is the disputed tax amount, and does the pre-deposit make commercial sense?

• Were principles of natural justice violated (e.g., no personal hearing under Section 75(4))?

A qualified CA or tax advocate can assess merit and help you make this decision. At PGA & Co., we offer a free 30-minute case assessment for this purpose.

Step 2: Calculate and Pay the Pre-Deposit

This is where most appellants make mistakes. The pre-deposit rules are:

• Cumulative 20%: You must pay 20% of the disputed tax in total — 10% was paid at the first appeal stage (Section 107), and an additional 10% is payable at the GSTAT stage (Section 112(8)).

• Electronic Cash Ledger or credit ledger : Payment of Pre-deposit can be paid through the Electronic Credit Ledger as well pursuant to ruling of Union of India vs Yasho Industries 2025 (92) G.S.T.L. 498 (Guj.) on the GST portal. However, some high courts have also given a contrary view to this fact and at present, the utilisation of Credit for making pre-deposit stands valid as per Supreme Court ruling.

• Cap: ₹20 crore each for CGST and SGST.

• Penalty-only appeals: For appeals filed after October 1, 2025 involving only penalties, the pre-deposit is 10% of the penalty amount.

Example: If the First Appellate Authority confirmed a demand of ₹7 crore CGST, your total pre-deposit is ₹1.4 crore (20% of ₹7 crore). If you already paid ₹70 lakh at the first appeal, you need to pay an additional ₹70 lakh before filing at GSTAT.

Step 3: Prepare Your Documents

The GSTAT portal requires ALL documents at the time of filing. You cannot add documents later (except with Tribunal permission). Based on the March 10, 2026 instructions from the GSTAT Registrar, the mandatory documents are:

• Show Cause Notice (SCN) — soft copy in PDF

• Order-in-Original (OIO) — soft copy in PDF

• Order-in-Appeal (OIA) — certified copy of the impugned order

• Statement of Facts — a factual chronology of the case

• Grounds of Appeal — consecutively numbered legal and factual grounds

• All relied-upon documents (invoices, returns, reconciliations, correspondence)

• Fee payment receipt from Bharatkosh

• Board resolution / authorisation letter (for companies and LLPs)

• Vakalatnama if represented by an advocate

• Verification document APL-02A

File size limit: Each PDF upload must be under 20 MB. Scan at 300 DPI or less. If documents are large, create multiple volumes.

Step 4: File on the GSTAT Portal

All appeals are filed electronically at efiling.gstat.gov.in using Form GST APL-05. The process:

1. Register on the portal with your authenticated email and mobile number

2. Validate your filing slot using the ARN/CRN of your APL-01/APL-03 filed at the first appeal stage

3. Complete all tabs: Order Details, Case Details, Appellant & Respondent Details, Add Representative, Demand Details

4. Upload all documents in PDF format

5. Pay the appeal fee via Bharatkosh (₹1,000 per ₹1 lakh of disputed tax, minimum ₹5,000, maximum ₹25,000)

6. Sign using Class II/III Digital Signature Certificate (DSC) or Aadhaar e-Sign

7. Submit and receive the provisional acknowledgement (16-digit filing number)

The portal issues SMS and email confirmation. Track your filing status on the dashboard under the ‘Refiling’ tab if defects are raised.

Step 5: Rectify Defects (If Any)

The GSTAT Registrar’s January 2026 office order provides a lenient scrutiny period during the initial phase — defects of form (not substance) will be overlooked. However, substantive defects like incorrect pre-deposit, missing grounds of appeal, or wrong jurisdiction will result in rejection.

If defects are raised, you’ll receive a notification to rectify. Only after defects are cleared will the Final Acknowledgement (Part B of APL-02A) be issued, and this is when your appeal is officially considered filed.

After Filing: What to Expect

• Hearings: Conducted in hybrid mode — you can attend physically or virtually. Limited to 3 adjournments.

• Sequence: Appellant is heard first, then respondent, with an opportunity for rejoinder.

• Orders: Uploaded on the GSTAT portal within 30 days of hearing. Certified copies provided to both parties.

• Rectification: The tribunal can rectify apparent errors within 3 months of the order.

• Ex-parte proceedings: If you fail to appear, GSTAT may proceed ex parte. You can apply for restoration if you show sufficient cause.

Common Mistakes to Avoid

1. Waiting until June to file. Portal glitches and document preparation take 4–6 weeks for complex appeals. Start now.

2. Using Cash ledger for paying pre-deposit and not using ITC as per Supreme Court Ruling in Yasho Industries.

3. Filing a combined appeal for multiple orders. Each Order-in-Original needs a separate Form APL-05.

4. Incorrectly claiming the case involves a Place of Supply issue. POS matters go only to the Principal Bench. Wrong jurisdiction = rejected appeal.

5. Not uploading a Vakalatnama when represented by an advocate. This is now mandatory.

When Should You Hire a CA or Tax Advocate?

You can file a GSTAT appeal yourself. But given the stakes — pre-deposit commitments, one-shot document uploads, and no facility to revise grounds after filing — professional help is strongly recommended for disputes above ₹5 lakh.

A qualified professional will:

• Assess merit and advise whether the appeal is commercially justified

• Draft legally sound grounds of appeal with relevant case law

• Calculate pre-deposit correctly and ensure payment is made through the right channel

• Handle portal technicalities and defect rectification

• Represent you during the hearing

At PGA & Co., our GST litigation team has Ex-Big 4 experience handling complex indirect tax disputes. We currently represent clients in GST matters across Chandigarh, Punjab, Haryana, and Delhi NCR.

Frequently Asked Questions

Need expert guidance on this topic?

PGA & Co. Chartered Accountants can help. Speak with our team today.